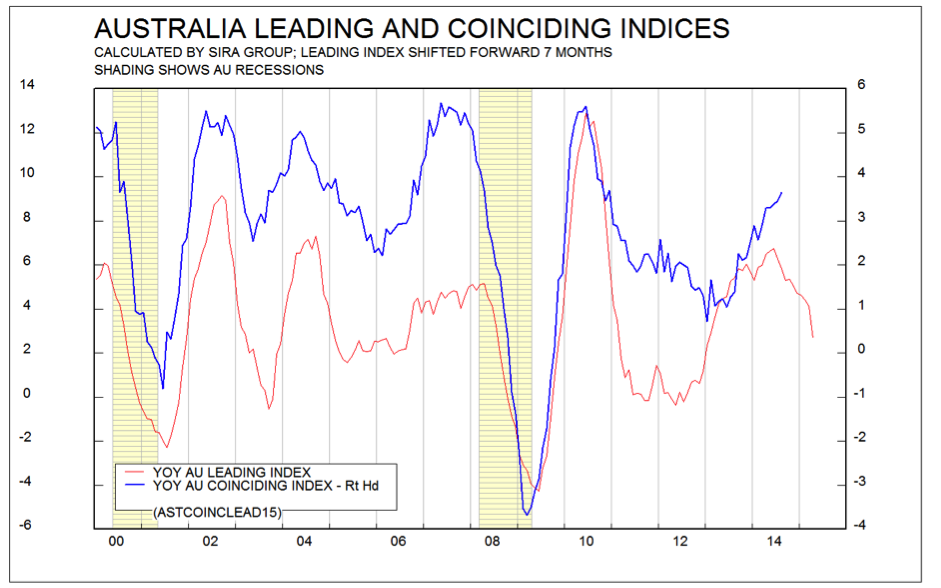

The SIRA Australian leading index, which is designed to “lead” the economic cycle, continues to weaken, calculated on a year-on-year percentage change basis. This provides an implicit forecast of what could happen to the real economy, represented here by the SIRA coinciding index (so called because it coincides with the cycle). We introduced our Australian leading and coinciding indices here.

In the chart below, the leading index (the red line) had been plotted with a 7 month lag, i.e., it has been shifted forward by seven months.

The decline in the leading index points towards a period of slow growth in the Australian economy. This is perfectly consistent with the weakness in commodity prices (the iron ore and coal prices have fallen by half over the last 4 years); the decline in mining investment as projects are completed; and weakness in consumer and business confidence. Until recently, the strength of the Australian dollar has also been a negative factor.

Even though SIRA’s leading index is weak, it’s not falling precipitously, as it did during the GFC (2008). So the economy will be weak, but a recession seems (at this stage) unlikely. All the same, the economy will likely be weaker than it has been since the GFC. And any stimulus from the fall in the Australian dollar could take several months to work through to the real economy.