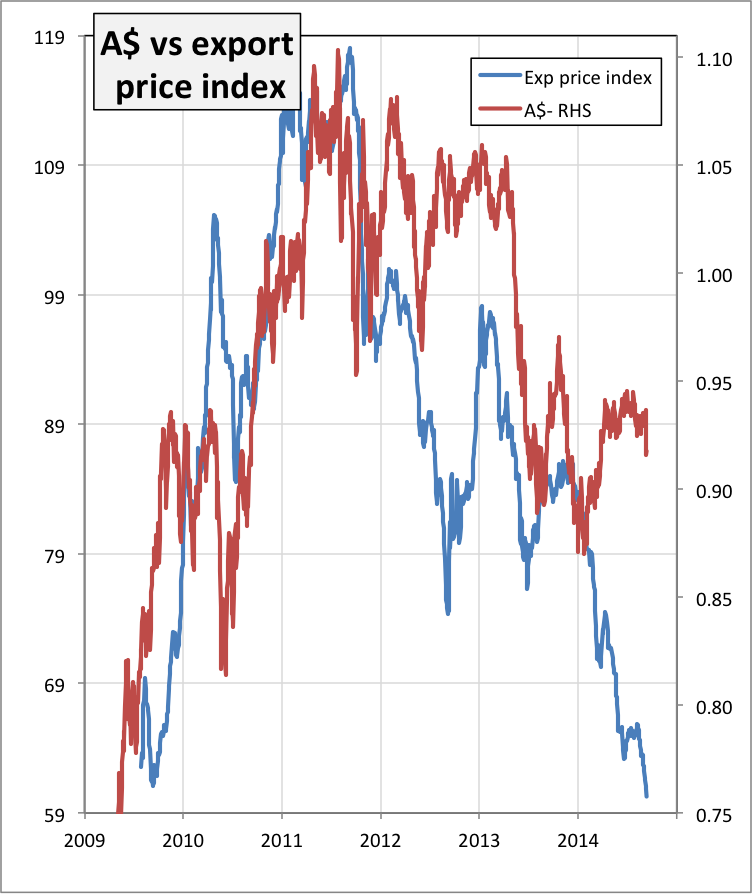

Over the last couple of years, the prices of Australia’s main commodity exports (coal and iron ore) have plunged. During the same period, however, the Australian dollar has held up surprisingly well against other currencies. Usually, over the last 30 years, when commodity prices have fallen, so has our currency, and that has helped cushion us against world recessions. That was after all one of the key reasons the A$ was floated back in the early 70s.

But what happens if the A$ doesn’t fall, even if commodity prices crash? Well, just as it used to be under fixed exchange rates, that’s a big negative for the economy. We have already seen some of the consequences of that in economic indicators which suggest that the economy is starting to slow.

But what happens if the A$ doesn’t fall, even if commodity prices crash? Well, just as it used to be under fixed exchange rates, that’s a big negative for the economy. We have already seen some of the consequences of that in economic indicators which suggest that the economy is starting to slow.

Why has the A$ held up, even while our terms of trade have deteriorated sharply? The answer is that our interest rates, relative to those elsewhere, such as Europe, Japan, the U.S., and the U.K., are high. This makes our government bonds and even short term deposits in Australian dollars attractive. So money flows into our currency, holding it up, and keeping it stronger than it would otherwise be.

The solution seems obvious, only it isn’t. That solution is for the RBA to cut the cash rate, which would help reduce the whole spectrum of interest rates. But house prices in Melbourne and Sydney are already rising rapidly, and a further cut in the cash rate and therefore the mortgage rate would stimulate the housing market more, risking the development of a housing bubble. Financial bubbles always end in tears, and the most important lesson learned by central bankers after the GFC is not to let them start in the first place. So it is very unlikely that the RBA will cut the cash rate, unless it can come up with a workable way to isolate the housing market from falling rates in the rest of the economy.

Fortunately, the US is moving steadily closer to raising its interest rates as its economy strengthens, which would help reduce the A$ against the greenback, and which is perhaps one of the reasons that the A$/US$ rate weakened over the last few days. Unfortunately, the US$ is rising against most major currencies except the Chinese Yuan, which means that even though we are falling against the US$, we are still holding up against the Euro, the Yen and the Pound. The “trade-weighted” dollar, which shows the A$ strength against a basket of currencies weighted by our trade patterns, is not falling, though it is at least not going up as fast as it was.

It sounds wonderful to have a strong currency. And so it is, if your economy is also strong. But when the economy is sluggish it is a mixed blessing.