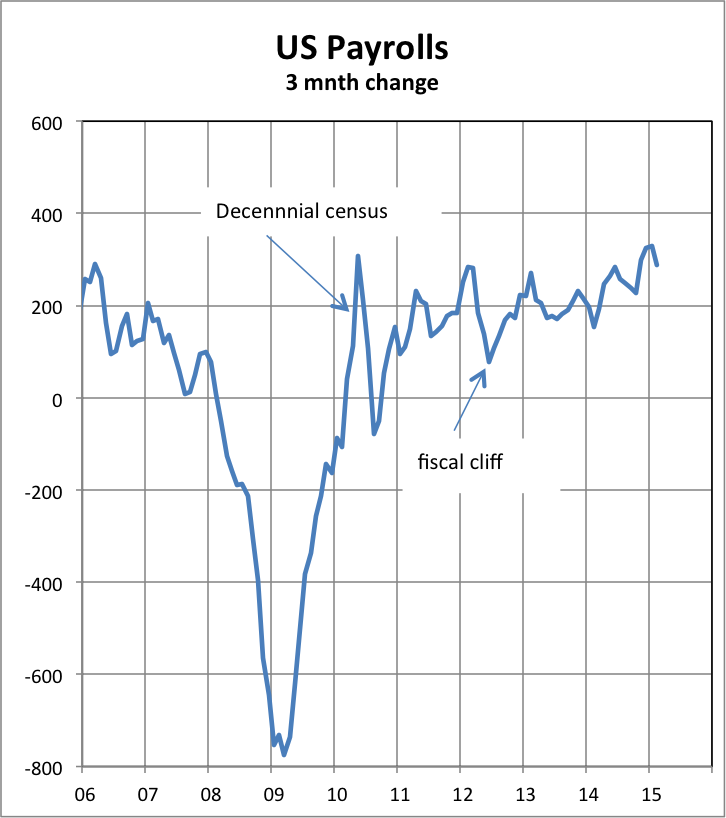

US employment data for February continued the strengthening trend of the last year, despite very cold weather over much of the eastern US and unseasonably warm weather/drought over the rest of the country. This was the highest increase in the three month average in a decade, if you ignore the short-lived spike when the US Federal Government hired a couple of hundred thousand temporary workers to take the ten-year census in 2010. In fact, it was close to the highest in three decades.

The US share market fell. But hang on, surely if times are good and getting better, surely the market should have gone up? Well, no. Because the stockmarket is a resultant (thinking of vector algebra here) of earnings, confidence and interest rates. And this strength in employment suggests that interest rates in the US will start to rise soon. For 6 years, the central bank discount rate (the “Fed Funds” rate) has been near zero, as the Fed tried to get economic growth going again after the GFC. And a rule of thumb is that a “neutral” discount rate/cash rate should be roughly equal to nominal GDP growth, which in the US over the last year has been around 4% per annum. A stimulatory rate would be below nominal GDP growth, a contractionary rate above it. After strong and prolonged stimulus, it is now necessary to raise interest rates to more normal levels to prevent future asset price bubbles and rising inflation. What these strong data suggested was that the probability of that happening has risen.

The US share market fell. But hang on, surely if times are good and getting better, surely the market should have gone up? Well, no. Because the stockmarket is a resultant (thinking of vector algebra here) of earnings, confidence and interest rates. And this strength in employment suggests that interest rates in the US will start to rise soon. For 6 years, the central bank discount rate (the “Fed Funds” rate) has been near zero, as the Fed tried to get economic growth going again after the GFC. And a rule of thumb is that a “neutral” discount rate/cash rate should be roughly equal to nominal GDP growth, which in the US over the last year has been around 4% per annum. A stimulatory rate would be below nominal GDP growth, a contractionary rate above it. After strong and prolonged stimulus, it is now necessary to raise interest rates to more normal levels to prevent future asset price bubbles and rising inflation. What these strong data suggested was that the probability of that happening has risen.

Now, it may happen that interest rates can rise (slowly!) but earnings may rise too, in which case the stockmarket will go sideways or even up. This often happens in the middle of an economic recovery. But later on in the recovery, earnings growth becomes harder to achieve, and the annual increases in profits slip. If interest rates start rising then, PE compression (a falling price-earnings ratio) overwhelms the rise in earnings, and the market falls. In addition, in the case of the US share market, a big chunk (30% plus) of profits are generated abroad (think of all the multinationals which dominate the Dow and the S&P). And since the US is so out of phase with the rest of the world, where interest rates won’t be rising any time soon, the US$ is soaring, reducing foreign profits when they are converted to US$. The market isn’t going to be rescued by a rise in earnings.

So this may mark the peak in the current bull market run in the US. We don’t think the fall will be substantial, but it is possible that it will qualify as a “bear market”, traditionally a 20% or more decline. The harder question is whether the Australian share market will fall too. Right now, we think not, because whereas the US is about to enter a period of rising rates, Australian interest rates are likely to fall further, while the decline in the A$ will help support earnings of listed Australian companies.