Economic indicators in Europe are showing signs of life!

The reason this i such an exciting event is that the European economy has more or less stagnated for 7 years. Real (inflation-adjusted) GDP for the EU as a whole is still below the pre-GFC peak in Q1 2008, after a series of policy blunders by the ECB (European Central Bank) and by the EU and key European governments.

The reason this i such an exciting event is that the European economy has more or less stagnated for 7 years. Real (inflation-adjusted) GDP for the EU as a whole is still below the pre-GFC peak in Q1 2008, after a series of policy blunders by the ECB (European Central Bank) and by the EU and key European governments.

This stagnation has eventually forced the ECB to act, though the politicians are still arguing about fiscal stimulus, which is also needed. The ECB introduced a program of QE —“Quantitative Easing”— which involves buying government bonds and paying for them with “printed” money (in other words with an expansion of the ECB’s own balance sheet.) At the same time, the Fed (The Federal Reserve Bank of the United States) has ended its own program of QE, and hinted that it might start raising interest rates. This has caused the US dollar to soar against the Euro, which has helped the European economy start to recover. When a country’s currency is devalued, it makes exports from that country cheaper in other countries and its imports from the other countries more expensive, thus stimulating the economy.

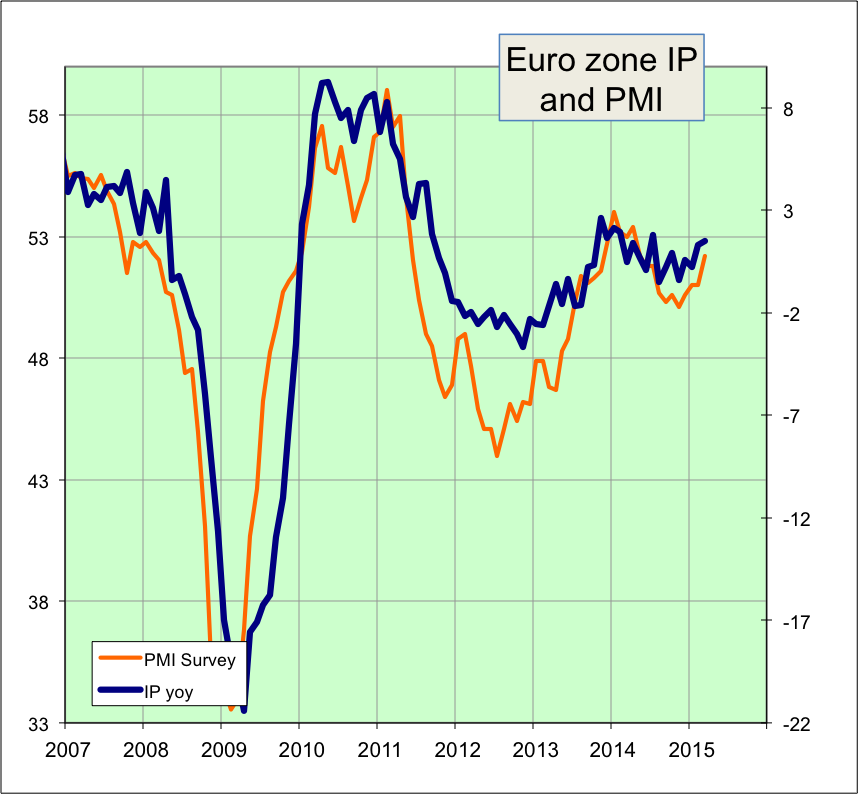

The chart above shows the year-on-year percent change in European industrial production, compared with the PMI index (which is an index derived from an opinion survey covering sales, profits, etc. of 5000 European companies). As can be seen, both have started to turn up, and this rise is likely to continue for now.

However, even though growth has resumed in Europe, the rate of growth is unlikely to be spectacular. Europe has too many serious structural problems, starting with an aging population and sclerotic labour market structures and ending with excessive government debt, to grow rapidly. Still, even small positives are an improvement over the dismal performance of the last 7 years.

Ironically, the US economy in recent months has slowed. Much of this is due to bad weather; some, however, is undoubtedly a response to the strengthening US dollar. So, some of the strengthening in Europe is at the expense of weakening in the US.

Over 7 years after the GFC crisis, caused by excessive and imprudent lending in the US, its consequences are still with us.